The report showing the average number of employees of the enterprise can be called not the main one in 2019, but very important, since the data provided in it will affect both the rest of the reporting and the calculation of tax amounts payable. Proof of eligibility for a particular system of taxation also lies with this document.

The form of the report on the average headcount in the form KND-1110018 can be downloaded at.

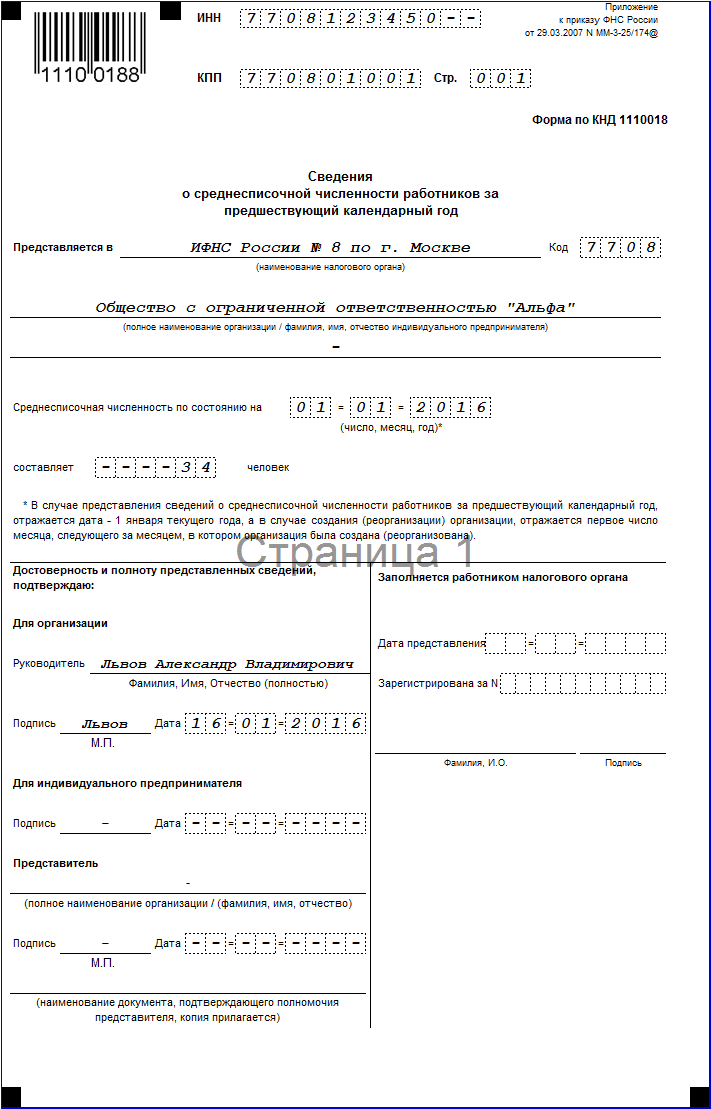

A sample of filling out for submission to the tax office can be seen in this image:

This document is submitted in the form of a form (KND 1110018), which indicates the exact data on the enterprise itself, as well as the results of calculations of the average number of workers for the year under study.

The calculations themselves are carried out in accordance with the requirements established by Rosstat, as well as the Tax Code. That is, legally, this indicator is calculated on the basis of the average number of employees of this enterprise for each month of the year. Moreover, the monthly indicator contains data on the number of employees employed part-time and full-time.

Reporting KND 1110018 "Information on the average number of employees" must be submitted to the tax authorities in electronic form if the headcount indicator is 100 or exceeds this value. Otherwise, organizations and individual entrepreneurs have the right to submit the form in paper form.

It should be noted that the report on the average headcount for the past year is submitted before January 20 of the current year.

It is necessary to submit the above report to those individual entrepreneurs who have employees, as well as to all legal entities.

The form for filling out is provided by both official and unofficial resources, it is important to simply observe the temporary relevance of the form.

Fill Features

The form according to KND 1110018 on the average number of employees must be filled out exclusively in black ink. Fill out the form legibly, in capital block letters, without corrections, errors, overwriting. The ideal filling option is a computer font, standard for documents, in size 18.

The population indicator is always filled with an integer. If after the calculations you received a fractional value, then it must be rounded according to mathematical rules - if after the decimal point 5, then one is added to the value before the decimal point, if less than 5, then the value before the decimal point is left unchanged. It is worth knowing that only the annual total is rounded, you cannot round employee data or monthly data.

Another feature of the report to the tax on the average headcount is that the date is indicated on January 1 of the new year, despite the actual date of its compilation. After all, the entrepreneur needs to display the status of employees on January 1.

Also, the responsible person should be careful not to accidentally fill in the columns intended to be filled in by the inspector.

For the calculation of the average headcount, see the detailed video:

Other input information

The report on the average number of employees in 2019 also has other information about the object of entrepreneurial activity, which must be correctly indicated:

- Code of the tax authority. Use the code assigned to the tax authority at the place of registration of the organization or at the place of residence of the individual entrepreneur, that is, the one where you will submit reports.

- TIN. This code is assigned to an object of entrepreneurial activity during registration with the tax office. It must be entered from left to right. In some cases, the entered TIN has fewer digits than the number of cells intended for them, then zeros are put at the beginning instead of the missing digits.

- Checkpoint. This column is important only for organizations. For IP, such data is not provided.

- Names. When indicating the name of the tax authority, the filler has every right to use an abbreviation, but never in relation to the name of the organization. It must be entered as it is written in the statutory documents.

- The entrepreneur writes his full name in the above field, there can be no abbreviations here. In the event that the submission of the document will be carried out by his authorized representative, it is necessary to enter the full name and an identity document.

A responsibility

The report on the average headcount for 2017 must be submitted by a certain date (January 20). This should be taken into account if you are going to send a document by mail.

Failure to comply with the above deadline will result in a fine. Moreover, if for an individual entrepreneur this is a relatively small amount of 200 rubles, then for an organization the fine can be increased, and 300-500 rubles of a fine can be added to the 200 rubles for the responsible person or the head of the facility.

So, the form of the form of the average number of 2017 includes not only the information on the number itself in the form of an integer, but also other information about the reporting object, entering which, it is necessary to follow a certain procedure and rules.

The indicator of the average headcount reflects information about the number of the payroll of the organization for a certain period. This value is used for tax and statistical accounting. This article discusses the question of in which cases the average number of employees is zero, and also provides a sample of information about the average number of employees is zero.

In what cases is it necessary to provide information on the average headcount

Information on the average headcount for the year as an independent reporting form is submitted to the tax authority annually, no later than January 20 of the current year. This requirement, established in accordance with paragraph 3 Art. 80 of the Tax Code of the Russian Federation, applies to both organizations and individual entrepreneurs. In addition, the CHR indicator is calculated in the following cases:

- when filling in the field of the same name of the form RSV-1 PFR;

- when filling out the "number of employees" field of Form 4-FSS;

- when calculating the amount of income tax paid at the location of a separate subdivision (clause 2 Art. 288 Tax Code of the Russian Federation);

- when submitting declarations to the tax authority in electronic form (clause 3, article 80 of the Tax Code of the Russian Federation).

The average number of employees is zero

Theoretically, this indicator can be zero if the legal entity or individual entrepreneur has no employees. In practice, disputes often arise about how legitimate it is in these cases to submit information about the average number of employees 0 people. This is due to the lack of a common understanding of whether it is possible to regard an individual acting as an individual entrepreneur as an employee? A similar issue occurs in relation to a person who heads an enterprise without personnel. We will analyze each of these situations separately and find out when information on the average number of employees is issued in the zero form.

The average number of employees of IP without employees

At present, the position of the legislative bodies regarding individual entrepreneurs without employees is becoming unambiguous and boils down to the fact that an individual entrepreneur, having the right to be an employer, cannot perform this function in relation to himself. This point of view is reflected in the Letter of Rostrud dated February 27, 2009 No. 358-6-1 and in the Letter of the Ministry of Finance of the Russian Federation dated January 16, 2015 No. 03-11-11 / 665. Thus, an individual entrepreneur does not have the right to regard himself as a staff unit when submitting reports. This is due to the fact that the legislation does not provide for the conclusion of a bilateral agreement, which is an employment contract according to Art. 56 Labor Code of the Russian Federation, With myself. Accordingly, the individual entrepreneur is not entitled to appoint himself and the payment of wages. At the same time, the Tax Code does not require that an individual entrepreneur submit a form of information on the zero average number of employees.

Zero average number of LLC without employees 2019

In the absence of employees, a legal entity has two options. In the first option, a person who is not a founder holds the position of CEO, has an employment contract with the company and receives a salary. In this case, the director is the only employee of the enterprise, and therefore, zero reporting on the quantitative composition does not apply. In the second option, the founder independently performs the functions of a director. Opinions differ on this point. From the point of view of the Federal Service for Labor and Employment, the founder of the organization is not its employee, since the employment contract cannot be signed by the same person on the part of the employee and the employer (Letter of Rostrud dated 06.03.2013 No. 177-6-1 ). This means that the average number of employees is given zero reporting.

However, this opinion has opponents, based on the fact that, from a legal point of view, in this case, an employment contract is not concluded with oneself, but between a legal entity and an individual.

Terms and conditions for submission

In accordance with the requirement of the Tax Code of the Russian Federation, all enterprises submit information on the number of employees for the past year, regardless of whether the staff works for them or not (clause 3, article 80 of the Tax Code of the Russian Federation). Individual entrepreneurs submit reports only if they hired employees last year. For both employers, the deadline for submitting information to the tax authority is no later than January 20 of the current year. Enterprises created after the expiration of the specified period are not exempt from this obligation. The zero average number of employees when opening an LLC is reflected in the report, which is submitted “no later than the 20th day of the month following the month in which the organization was created (reorganized)” (clause 3, article 80 of the Tax Code of the Russian Federation). A similar requirement applies in the event of a reorganization of an enterprise that occurred after January 20.

Report Form

The corresponding form, called Form KND 1110018, was approved by Order of the Federal Tax Service of the Russian Federation of March 29, 2007 No. MM-3-25 / 174. The document, presented on one page, is simple enough to fill out. First of all, it contains information about the taxpayer (TIN, KPP, name of the tax authority, name of the organization or full name of the individual entrepreneur). Next, the date for which the NFR indicator is calculated and, in a separate column, its value in whole units is indicated. The date of submission of the report to the tax authority is entered in the lower left part of the document.

The form is signed by the head of the organization or individual entrepreneur. If necessary, the representative of the taxpayer can sign the signature if there is an appropriate power of attorney.

The average headcount for 2015 must be submitted in the form approved by Order No. MM-3-25/174 dated March 29, 2007.

Average headcount, form 2016

Calculate the average number of employees for 2015 as of January 1, 2016. This date and indicate the information about the average. At the same time, do not include persons working under civil law contracts (letter of the Federal Tax Service of Russia dated February 24, 2011 No. KE-4-3 / 2964).

You can calculate the average number of employees by following the Instructions approved by Rosstat Order No. 428 dated October 28, 2013 (hereinafter referred to as the Instructions). To determine the average number for the year, use the formula:

In cases where the company has been operating for an incomplete year (for example, it was registered in the summer), this indicator should be calculated in a similar way. That is, all the same, the sum of the average headcount for all months must be divided by 12 (paragraph 81.10 of the Instructions).

On a note! For failure to provide information, the company may be fined 200 rubles. (Clause 1, Article 126 of the Tax Code of the Russian Federation). A fine for an official is from 300 to 500 rubles. (part 1 of article 15.6 of the Code of Administrative Offenses of the Russian Federation).

If the company has separate divisions, it is necessary to determine the average number of employees for the whole organization (letter dated December 29, 2006 No. 03-02-07 / 1-364).

Average headcount for 2015. Sample

Who needs to submit information about the average headcount during the year

Newly created (reorganized) companies must submit information on the average headcount no later than the 20th day of the month following the month of creation (reorganization) (paragraph 3, clause 3, article 80 of the Tax Code of the Russian Federation, letter of the Federal Tax Service of Russia dated April 28, 2010 No. ShS-17-3/0103).

But for the first time registered individual entrepreneurs are exempted from this obligation. They submit information on the average headcount exclusively at the end of the year (letter of the Ministry of Finance of Russia dated July 19, 2013 No. 03-02-08 / 28369).

Any organization / individual entrepreneur in the process of activity is faced with the need to calculate the number. Information may be provided to external and internal users in a statutory or arbitrary form.

Dear readers! The article talks about typical ways to solve legal issues, but each case is individual. If you want to know how solve exactly your problem- contact a consultant:

APPLICATIONS AND CALLS ARE ACCEPTED 24/7 and 7 days a week.

It's fast and IS FREE!

Essence of the question

The number of employees is: list, average and average. For different purposes, you need to define different numbers. The average number is recognized as a general indicator - it most fully covers all categories of workers. The payroll is next, and the average payroll is calculated from it.

Reason for compiling

There can be several reasons for making a referral. The main one is the requirements of the tax legislation.

Employees of the IFTS determine which organizations / entrepreneurs must submit reports in paper form and which in electronic form based on the average indicator.

If the figure does not exceed 100 people per year, you can report on paper declarations. Therefore, all legal entities and entrepreneurs must report from 2008 for the previous calendar year on the average headcount. The certificate is also drawn up during the creation, reorganization, liquidation, closing of the enterprise.

The average number is used to confirm the right to the simplified tax system, the calculation of UTII for certain services, such as repairs, car washing, veterinary, household services. Also for preferential confirmation to organizations with disabled employees.

Information on the average headcount does not apply to declarations, therefore, failure to submit threatens the organization and executives with fines:

- at the rate of 200 rubles– for a legal entity or an entrepreneur;

- at the rate of 300 - 500 rubles- to an official.

In addition, certificates of headcount in any form may be needed by banks, credit institutions, company owners and other users.

Filing authorities

The average number in the form of a certificate is submitted by all taxpayers, regardless of the registration form:

- To the IFTS authorities until January 20 for the previous year. When a new legal entity is created or an old legal entity is reorganized, the certificate must be submitted by the 20th day of the month following the month of creation or reorganization. For example, the company was registered on May 18, you need to submit a certificate before June 20, reflecting information as of 01.06.

Who submits:

- enterprises of any tax regime and type of activity;

- individual entrepreneurs with employees.

Who does not apply:

- individual entrepreneurs without employees - from 01.01.2014 (Article 80 of the Tax Code of the Russian Federation). There is no need to report for 2013.

The certificate is submitted at the place of registration of the entrepreneur or at the place of registration of the head office of the organization.

- The FSS and the PFR also provide information on the payroll as part of the calculations of 4-fss and RSV-1.

- Information on the average number is submitted to the statistical authorities according to the forms P-4, PM, mp-micro, as necessary.

How is a certificate of the number of employees of the organization compiled? (sample)

The form of the form on the average headcount was approved by order of the Federal Tax Service of Russia dated March 29, 2007 No. MM-3-25 / [email protected] For correct filling, recommendations have been developed, which are given in the annex to the letter of the Federal Tax Service of Russia dated April 26, 2007 No. ChD-6-25 / 353a. KND form code 11100018.

When compiling a certificate, you must specify the following data:

- document's name;

- full name of the IFTS body;

- the full name of the legal entity or entrepreneur making the calculation;

- TIN/KPP;

- number as of the required date;

- date of filling out the form;

- transcript and signature of the official.

The form is filled in two copies: one - for the tax authority, the second remains with the filler with a mark and date of receipt.

Summing up, it should be noted that:

- the average headcount is submitted to the tax authorities in the form with the KND code 11100018.

- payroll data are provided to the FSS and the PFR;

- information on the size of the average is provided to the statistical authorities.

Average for the period

The calculation is made on the basis of information on the payroll, taken into account daily, according to the arithmetic mean formula, taking into account the required period - month, quarter or year. First, the indicator for the month is calculated, from it - quarterly and annual.

When calculating, one should be guided by the Decree of the Federal State Statistics Service No. 56 of October 09, 2006, which regulates the rules for assigning categories of workers.

To begin with, on the basis of timesheets, personnel documents, it is necessary to calculate the number. All employees are taken into account: those who are at work, sick, absent.

The headcount does not include:

- business owners without wages;

- apprentice workers on the basis of a vocational training contract;

- military;

- lawyers;

- employees registered under civil law contracts;

- persons who are abroad;

- employees sent to other enterprises and not receiving payment for their work;

- employees who applied for dismissal and stopped working earlier than the appointed date or without warning the administration;

- employees working under contracts with state enterprises;

- external collaborators.

The average payroll looks like this:

Included in the list:

- ordinary employees;

- seconded employees while maintaining pay for work, including employees who are seconded for a short time abroad;

- sick employees;

- government officials;

- truants;

- part-time or part-time employees. The running time is taken proportionally. Exception - categories of persons entitled to reduced hours of work in accordance with the law: minors; persons employed in hazardous conditions; nursing mothers; disabled people of groups I and II (in the calculation they are taken as 1);

- taken on probation;

- homeworkers;

- persons of special ranks;

- temporarily working employees of other enterprises, if the former does not retain wages;

- practicing students, if they are issued according to the Labor Code;

- employees on additional leave for training and admission without pay are not taken into account when determining the average list data;

- replacement specialists;

- employees on leave without saving with the consent of management;

- striking employees;

- women on maternity or adoption leave are not taken into account when determining the average list data;

- employees who take leave for study and receive wages;

- employees on vacation in accordance with the Labor Code, including those leaving after vacation;

- persons on leave;

- shift workers;

- Foreigners;

- persons under investigation.

When calculating information for a month, it is necessary to sum up the daily indicators, taking into account that days off and holidays are taken from the last working day before them. Then the figure is divided by the number of days of the month according to the calendar and rounded up to a whole number.

Information for the quarter/year is calculated as follows: the information for all months is summed up and divided by 3/12. The final total must be rounded to the nearest whole number; in this case, the subtotal for the month does not need to be rounded.

Documents that may be needed when calculating data:

- hiring/dismissal orders;

- vacation and transfer orders;

- travel orders;

- personal cards of employees;

- time sheet;

- payroll calculations;

- statements containing information on payments and settlements.

See also the video on submitting information about the average headcount

Established

Headcount is the number of employees of the enterprise according to the staffing table.

This term is used in business planning of headcount in managerial matters.

It can be enshrined in the statutory documents, but this mainly applies to government agencies, it is rarely used in commercial structures due to the complexity of this procedure.

It is calculated on the basis of labor standards, taking into account planned absenteeism according to accounting data.

Each company develops its own standards.

W \u003d H x Kn,

where W is the number of staff,

N - the number of normative,

Кн – planned absenteeism coefficient, defined as:

Kn = 1 + % absenteeism / 100

Often, normative data on the number are called secret data, and regular data are called list data. The list data must match the information from the timesheets that record attendance at the enterprise.

Rules for counting list data:

- All persons registered under employment contracts are taken.

- Owners who receive payment for work are taken.

- Both present and absent persons are taken.

- The data must match the data in the spreadsheets.

Medium

The average number is used in calculating various performance ratios: labor productivity, average wages.

The average also includes:

- Persons registered under civil law contracts. They are considered as ordinary employees accepted into the organization for the full time of work. Entrepreneurs are an exception.

- Companions of an external nature. They are counted as part-time workers. If you get a small digital indicator, leave one decimal place after the decimal point.

Average headcount \u003d average headcount + GPD employees + external part-time workers.

The nuances of the calculation

When calculating the number of employees, some features of the procedure should be taken into account:

- If an organization/entrepreneur operates for less than a full month, the number of calendar days per month is taken into account when calculating the headcount. Such a situation is possible with a new enterprise, with an enterprise operating seasonally. Example: an enterprise was registered on September 18 with 20 employees. September headcount \u003d (20 people x 13 days) / 30 days \u003d 8.66 people, rounded up to 9.

- If the organization/entrepreneur has been operating for less than a full year, when calculating, we still divide by 12 months.

- If there was a reorganization or liquidation procedure, it is necessary to take into account the data of predecessors when calculating.

- If work at the enterprise has been suspended, the general rules apply.

- If employees work part-time at will, then they are counted as a whole unit in the payroll, and in proportion to the time of work in the average payroll. At the same time, it should be remembered that if part-time work is related to the law or the initiative of the employer, then such persons are always counted as a unit.

part-timers

Accounting is conducted depending on the type of combination. Part-time employees of an internal nature are taken as a unit, regardless of the rate at which they are issued. Part-time employees of an external nature are not considered, since they are taken into account at the main job.

maternity leave

Persons on maternity leave are counted differently depending on the type of headcount.

When calculating the average list data, they are not taken, but are included in the payroll.

Partial rate

Employees transferred by management for part-time work or registered with a reduced work time (for example, disabled people, minors, nursing mothers) are taken as a unit.

Part-time employees of their choice are taken into account when calculating:

- in proportion to working time - when calculating the average list information;

- as a unit per day - when calculating list information.

When calculating the average headcount per month for part-time workers, the following formula should be used:

working time of such employees in hours per month total / duration in hours of a day of work / set number of days of work in a month.

For example, at 0.5 employee rate (with 20 working days in a month): 80/8/20 = 0.5

Temporary workers

Information on the average number of employees (form)

Calculation of the average headcount

The average headcount is determined in accordance with the requirements of Rosstat (Appendix No. 1 to Rosstat Order No. 580 dated September 24, 2014).

It is calculated based on the payroll. For each working day of the month, it includes employees, including those hired for temporary or seasonal work, both those present at their workplaces and absent, for example, for the following reasons:

- those on sick leave;

- sent on a business trip;

- who are on regular paid leave;

- who are on vacation at their own expense;

- who received a day of rest for working on a day off;

- working at home.

On a weekend or holiday, the headcount is considered equal to the headcount for the previous business day.

Who is not included in the payroll

The average headcount does not include:

- external part-timers;

- persons with whom civil law contracts are concluded;

- women on maternity leave;

- persons on parental leave.

Calculation at full employment of employees

The average number for the month is calculated according to the formula:

Calculation for part-time work

For employees working part-time under an employment contract, the average headcount is calculated using the following formula:

Sick days and vacation days of part-time employees are counted for the same number of hours as their previous working day.

Workers who work part-time at the initiative of the employer or by virtue of law, such as minors, are counted as whole units in the calculation.